Economic Affairs, Vol. 65, No. 4, pp. 665-674, December 2020

DOI: 10.46852/0424-2513.4.2020.25

![]()

Case Study

Costs and Returns Structure in Bottle Gourd on the Contract vis-a-vis Non-Contract Farms in the Jaipur District of Rajasthan

ABSTRACT

The present investigation was undertaken with a view to studying the costs and returns structure by the contract and non-contract farmers under contract farming of bottle gourd. Primary data were collected for the agricultural year 2015–16. The cost concepts were used. The results of the study revealed that all types of incomes viz., gross income, family labour income, farm business income and net income were higher on the contract farms than on the non-contract farms. The net income per hectare from bottle gourd was 31.69 per cent higher on the contract farms as compared to the non-contract farms. The total costs were higher on contract farms than on non-contract farms. The net profit was higher on contract farms than on non-contract farms. Returns per rupee were higher on contract farms (₹ 1.82) than non-contract farms (₹ 1.69).

Highlights

In bottle gourd cultivation the net income per hectare and returns per rupee was higher on the contract farms than the non-contract farms

In bottle gourd cultivation the net income per hectare and returns per rupee was higher on the contract farms than the non-contract farms

Keywords: bottle gourd, contract farming, gross income, net income

This study was related to contract farming revealed that the farmer's favoured contract farming because it provided them with better prices, gave them reliable incomes, generated employment especially for women, introduced improved practices of farming and did away with relationship between the large and small producers. India with vegetable production of 146.55 million tons is the second largest producer of vegetables contributing 14% of world's vegetable production in 2017–18. With an area of 10.4 million hectares under vegetables, the average productivity of vegetables in India was 17.3 t/ha in 2017–18. In Rajasthan 1.7 million ha area was under vegetable cultivation in 2017–18 with production of 17.675 tons and productivity of 6.3 t/ha. (Vegetable Statistics - IIVR (2017-2018). In Jaipur district Bassi, Jhotwara and Shahpura were the major blocks for the production of bottle gourd with an area and production of 125 hectares (360 qt/ ha), 65 hectares (350qt/ha) and 50 hectares (350qt/ ha), respectively.

Productivity in agriculture can be increased through adoption of improved technology. Judicious use of resources coupled with proper technology plays an important role in stepping up agricultural production (Singh et al. 2006). It was generally noticed that the farmers were not using recommended level of crop production technology. This results in a gap between the potential and actual yield. In the production of bottle gourd, farmers and contracting firms face many problems like transfer of technology, supply of quality seed, arrangements of institutional credit, fertilizers and other inputs, market arrangements, timely payments, violation of terms and conditions, lack of proper management by the company, frequent price fluctuations in markets, lack of transport facilities during peak periods, etc.

How to cite this article: Rajput, A.S., Sharma, V. and Sharma, R.C. (2020). Costs and Returns Structure in Bottle Gourd on the Contract vis-a-vis Non-Contract Farms in the Jaipur District of Rajasthan. Economic Affairs, 65(4): 665–674.

Source of Support: None; Conflict of Interest: None ![]()

Examination of costs and returns in agriculture plays a significant role in making the farm sector economically viable and feasible under the pressure of continuous rise in input prices (Kale et al. 2005). The level of input use and their prices affect the profitability of the crop enterprise. This mechanism needs to be critically examined for formulating effective policies in relation to costs and output prices for understanding the income path in the farm sector. As such there was a need to study the costs of and returns on different size-groups of contract and non-contract farms in the Jaipur district.

DATABASE AND METHODOLOGY

In Jaipur district contract farming in case of cucurbits was prevalent only in three tehsils namely Bassi, Jhotwara and Shahpura. Among these three tehsils, Bassi tehsil ranks first in area and production of bottle gourd. Therefore, bassi tehsil was selected purposively for the study purpose. Multi stage stratified random sampling technique was used for drawing a sample for the present study. A list of 26 villages having contract farming in bottle gourd was obtained from the Bassi tehsil. Three villages namely Dhindon, Damodarpura and Kacholiya were selected randomly. Out of 127 bottle gourd growers (57 were contract farmers and 70 were non-contract farmers), 50 farmers were selected randomly for the study of which, 30 were contract and 20 were non-contract farmers.

The costs and returns of bottle gourd were analyzed for the contract and non-contract farmers to examine the economics of crop production. The cost concepts used for estimating costs, gross returns and net returns in respect of bottle gourd crop are given below:

Cost concepts

Costs were computed by following certain cost concepts and items of costs (all measured in monetary terms) as discussed below:

Cost A1:

(i) Value of hired human labour

(ii) Value of hired bullock labour

(iii) Value of owned bullock labour

(iv) Value of owned machinery

(v) Hired machinery charges

(vi) Value of seed (both farm produced and purchased)

(vii) Value of manures (both farm produced and purchased)

(viii) Value of fertilizers

(ix) Value of insecticides and pesticides

(x) Irrigation charges

(xi) Depreciation on farm buildings and implements

(xii) Interest on working capital

(xiii) Insurance premium

(xiv) Land revenue

(xv) Miscellaneous expenses

Cost A2: Cost A1 + rent paid for leased-in land

Cost B1: Cost A1+ interest on fixed capital (excluding land)

Cost B2: Cost B + rental value of owned land + rent paid for leased-in land

Cost C1: Cost B1 + imputed value of family labour

Cost C2: Cost B2 + imputed value of family labour

Cost C3: Cost C2 + 10 per cent of cost C2 as management cost

Rental value of owned land

It was calculated on the basis of prevailing rates in the sample villages i.e., ₹ 10000 per year.

Depreciation: Depreciation on an asset was calculated using the straight line method:

Cost of production (per quintal) - Cost of production was worked out by using following formula:

Operational cost (O.C.) - It is the variable cost that varies with the level of production. It was expressed as:

OC = Cost A1 - Land revenue - Depreciation + Family labour charges

Overhead cost (O.H.C.)

Overhead cost or fixed costs were the sunk costs which had no bearing on the size of production. These were calculated by subtracting variable costs from the cost C2. In other words,

OHC = Cost C2 - Variable costs

Gross income

Synonymous with value of output (both main product and by-product) evaluated at harvest prices. Symbolically:

GI = Qm × pm + Qb × Pb

where,

GI = Gross Income; Qm = Quantity of main product; Pm = Price of main product; Qb = Quantity of byproduct; pb = Price of by-product

Family labour income (FLI) - It is the return to family labour (including management).

Net income (NI)

NI = Gross income - Total cost (Cost C2)

Farm business income (FBI) - It is the disposal income out of the enterprise and is defined as:

FBI = Gross income - Cost A1 (cost A2 in case of tenant operated land)

Return per rupee (RPR)

RESULTS AND DISCUSSION

Costs and returns structure

This sub section deals with the economics of bottle gourd crop production during zaid based on utilization of farm inputs.

Utilization of farm inputs in physical quantity in bottle gourd on contract farms

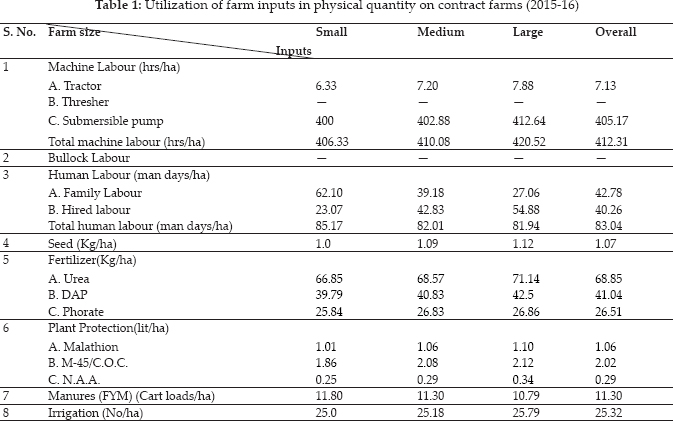

The table 1 indicates that the utilization of machine labour varied from 406.33 hrs/ha on small farms to 420.52 hrs/ha on large farms. Overall machine labour utilization was 412.31 hrs/ha. Utilization of total human labour was highest (85.17 man days/ ha) on small farms and lowest (81.94 man days/ha) on large farms. Overall utilization of human labour was estimated at 83.04 man days/ha which was more than that utilized on medium and large farms.

Utilization of farm inputs in physical quantity in bottle gourd on non- contract farms

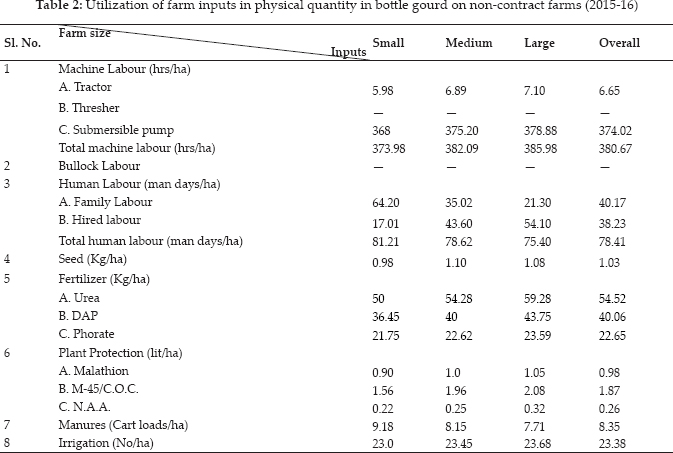

The table 2 indicates that the utilization of machine labour was highest (385.98 hrs/ha) on large farms followed by medium (382.09 hrs/ha) and small (373.98 hrs/ha) farms. Overall machine labour utilization was 380.67 hrs/ha.

Utilization of family labour varied from 21.30 man days/ha on large farms to 64.20 man days/ha on small farms with an overall family labour utilization of 40.17 man days/ha. Utilization of hired human labour varied from 17.01 man days/ha on small farms to 54.10 man days/ha on large farms with an overall hired labour utilization of 38.23 man days/ha. Utilization of family labour was inversely related with hired human labour. It decreased with the increase in size of farms. In case of hired human labour the trend was just reverse. Utilization of total human labour varied from 75.40 man days/ha on large farms to 81.21 man days/ha on small farms with an overall human labour utilization of 78.41 man days/ha in the study area. Lesser utilization of human labour on large farms was attributable to more use of machine labour on such farms.

Utilization of farm inputs in monetary terms in bottle gourd on contract farms

The table 3 indicates that on contract farms, miscellaneous expenses occupied a lion's share (32.74 per cent) in the total cost of cultivation for bottle gourd 90979.51). The next major component of cost was irrigation charges which accounted for 7.13 per cent of the total cost. The irrigation charges increased with small farms 6250) to the large farms 6720). The family labour charges were higher ₹ 15525 on small farms as compared to that on large farms 6765) - overall charges being ₹ 10695 per hectare.

Utilization of farm inputs in monetary terms in bottle gourd on non- contract farms

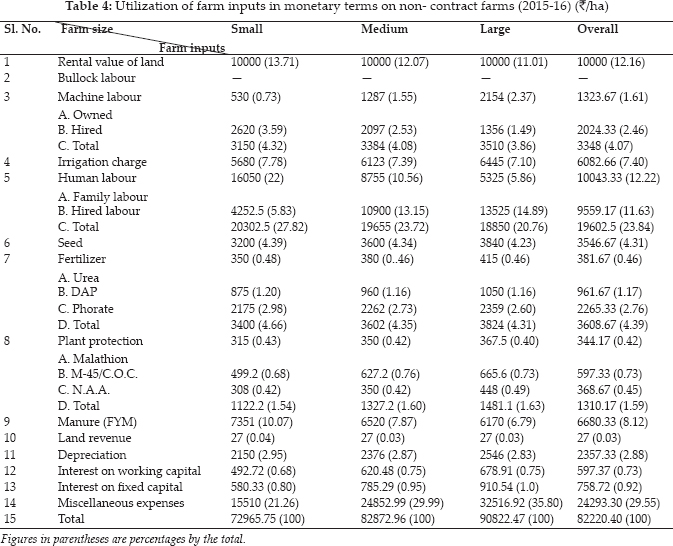

The table 4 indicates that the rental value of land 10000) occupied (12.16 per cent) share in the total cost of cultivation 82220.40). Irrigation charges with 7.40 per cent followed by human labour (23.84 per cent), manure (8.12) and miscellaneous expenses (29.55) stood next as major cost components. Family labour and hired human labour charges inversely varied with the size of holding. Per hectare expenditure on human labour decreased with the increase in the size of farms in the study area.

Fertilizer cost increased with the increase in size of farms due to lesser availability of manures on large farms. Interest on working capital and fixed capital jointly accounted for 1.65 per cent of the total cost.

Comparative economics of bottle gourd cultivation on contract and non-contract farms

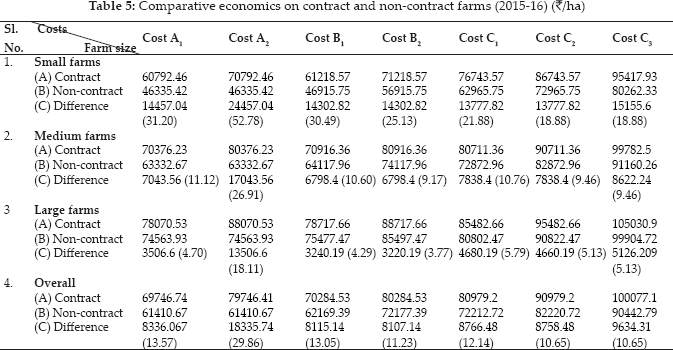

The table 5 indicates that overall costs A1, A2, B1, B2, C1 and C2 on contract farms were worked out at ₹ 69746.74, ₹ 79746.41, ₹ 70284.53, ₹ 80284.53 ₹ 80979.20 and ₹ 90979.20, respectively. These respective costs were higher by ₹ 8336.06, ₹ 18335.74, ₹ 8115.14, ₹ 8107.14, 8766.48 and ₹ 8758.48 on contract farms than on non-contract farms. Cost A2 was more than to cost A1 as farmers of the contract farms had leased in land. Magnitude of cost C2 was ₹ 86743.57 on small farms of contract farms as against ₹ 72965.75 on non-contract small farms.

The difference of cost C2 was more on non-contract farms 125981.21) than contract farms 105769.50). These costs increase with increased of size of holdings. These results were in confirmity with Dileep et al. (2002), Singh et al. (2006) and Kumar et al. (2019).

The variation in all the cost concepts on contract and non-contract farms was due to the variation in the input use and investments made in farm assets by the selected contract and non-contract farms. These findings were in confirmity with Dileep et al. (2002), Tripathi et al. (2005) and Singh et al. (2006). The cost differences between contract and non-contract farms were observed higher on small farms followed by medium and large farms because of less investment and low risk bearing capacity of the non-contract farms in respective categories.

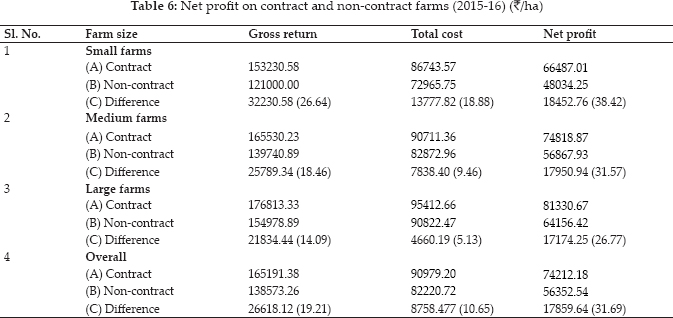

Net profit from the cultivation of bottle gourd on contract and non- contract farms

The table 6 indicates that overall gross returns, total Costs and net profit on contract farms were worked out at ₹ 165191.38, ₹ 90979.20 and ₹ 74212.18 per hectare, respectively. These parameters were higher by ₹ 26618.12 (19.21 per cent), ₹ 8758.48 (10.65 per cent) and ₹ 17859.64 (31.69 per cent) than on non-contract farms.

The overall gross return was higher on contract farms 165191.38) than the non-contract farms (₹ 138573.26). The total costs incurred on cultivation of bottle gourd were higher on contract farms than on non-contract farms. The total cost of cultivation on contract farms was higher due to more use of farm inputs than on non-contract farms.

The net profit was higher on contract farms 74212.18) than on non-contract farms 56352.54). This was attributable to realization on higher price and more physical output than on non-contract farms. These results were in confirmity with Singh et al. (2006) and Sivagami et al. (2010).

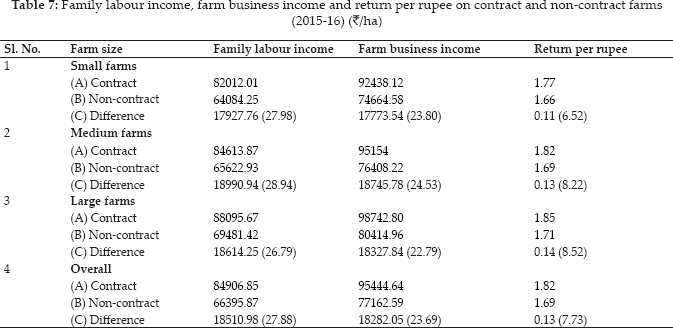

Family labour income, farm business income and returns per rupee from the cultivation of Bottle gourd on contract and non- contract farms

The table 7 indicates that overall family labour income, farm business income and returns per rupee on contract farms were worked out at ₹ 84906.85, ₹ 95444.64 and ₹ 1.82 per hectare, respectively. These parameters were higher by ₹ 18510.98 (27.88 per cent), ₹ 18282.05 (23.69 per cent) and ₹ 0.13 (7.73 per cent) than on non-contract farms.

Category wise family labour income varied from ₹ 82012.01 on small farms to ₹ 88095.67 on large farms under contract farms and from ₹ 64084.25 to ₹ 69481.42 on non-contract farms. Similarly farm business income ranged from ₹ 92438.12 on small farms to ₹ 98742.80 on large farms under contract farms and from ₹ 74664.58 to ₹ 80414.96 on non-contract farms. Returns per rupee ranged from ₹ 1.77 on small farms to ₹ 1.85 on large farms under contract farms and from ₹ 1.66 to ₹ 1.71 on the same categories of non-contract farms. Returns per rupee was higher on contract farms 1.82) than noncontract farms 1.69). The family labour income, farm business income and returns per rupee were higher on contract farms due to higher production and price of the product. These findings were in confirmity with Singh et al. (2006).

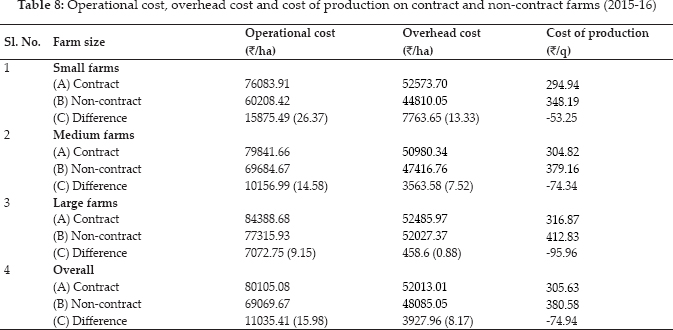

Operational cost, overhead cost and cost of production from the cultivation of bottle gourd on contract and non- contract farms (2015-16)

The table 8 indicates that overall operational cost, overhead cost and cost of production on contract farms were worked out at ₹ 80105.08, ₹ 52013.01 and ₹ 305.63 per hectare, respectively. These parameters were higher by ₹ 11035.41 (15.98 per cent), ₹ 3927.96 (8.17 per cent) and ₹ -74.94 than on non-contract farms.

Cost of production ranged from ₹ 316.87 on large farms to ₹ 294.94 on small farms under contract farms and from ₹ 412.83 to ₹ 348.19 on the same categories of non-contract farms. Category wise difference in cost of production between contract and non-contract farms was higher on small farms followed by medium and large farms. The operational cost and overhead cost were higher on contract farms than on non-contract farms due to more use of inputs. It increased with the increase in the farm size. These findings were in conformity with Singh et al. (2006) and Singh et al. (2020). The cost of production was noted to be higher on non-contract farms. It may be attributed to less use of inputs, low output and less price of the output on these farms as compared to that on contract farms.

CONCLUSION

Additional Comments

◆ The government should make adequate arrangement for timely supply of necessary inputs at reasonable prices to the growers so as to increase per hectare productivity as well as net returns.

◆ Bank credit and financial assistance should be available to the individual farmers for increasing the production.

◆ Training of farmers in the areas of production technology, grading, standardization of produce, quality control and modern method of marketing will prove to be a viable move.

◆ The government should establish adequate storages at village level for the purpose of orderly marketing of bottle gourd to benefit both consumers and producers.

◆ This study was helped the farmers in reducing the cost of cultivation by using appropriate techniques and tools and improve the net return of the farmers in the study area.

ACKNOWLEDGMENTS

This research paper is part of my MSc. research work at SKNAU, Jobner, Jaipur so I thankful to My Major Advisor Dr. R.C. Sharma and my advisor committee who help and support me for my research work.

REFERENCES

Anonymous, 2017-18. Economic Survey. Vegetable Statistics - IIVR

Anonymous, 2017-18. Vital Agricultural Statistics. Directorate of Economics and Statistic, Jaipur.

Dileep, B.K., Grover, R.K. and Rai, K.N. 2002. Contract Farming of Tomato: An Economic Analysis. Indian Journal of Agricultural Economics, 57(2): 197–210.

Kale, N.K., Navadkar, D.S. Gavli, A.V. and Sale, D.L. 2005. Resource Use Efficiency in Chilli Cultivation in Thane District of Konkon Region. Indian Journal of Agricultural Economics, 60(3): 529.

Kumar, R., Kumar, N., Dhillon, A., Bishnoi, D.K., Kavita and Malik, A.K. 2019. Economic analysis of guava in Sonepat district of Haryana. Economic Affairs, 64(4): 747–752.

Singh, B., Singh, R.K. and Gupta, R.K. 2006. Contract Farming in Potato Production (An Alternative of Rural Marketing) in District of Farrukhabad, Uttar Pradesh. Indian Journal of Agricultural Marketing, 20(3): 57.

Singh, H., Kaur, M. and Sekhon, M.K. 2006. Contract Farming in Punjab-A Strategy for Diversification. Indian Journal of Agricultural Marketing, 20(3): 40–41.

Singh, N., Sharma, R. and Kayastha, R. 2020. Economic analysis of pea in Himachal Pradesh. Economic Affairs, 65(2): 191–195.

Sivagami, R., Alagumani, T. and Samsai, T. 2010. Integration of Production and Marketing of Maize through Contract Farming- An Economic Analysis. Indian Journal of Agricultural Marketing, 24(2): 145–151.

Tripathi, R.S., Singh, R. and Singh, S. 2005. Contract Farming in Potato Production: An Alternative for Managing Risk and Uncertainty. Agricultural Economics Research Review, (Conference No. 18): 47–60.